Leave Encashment In India: Rules, Tax Exemption & Calculation (2026)

The four-factor calculation, the lifetime cumulative cap, and the regime-neutral exemption: everything HR leaders, payroll heads, and employees need before the next separation is processed.

Table of contents

One unstitched HR platform to manage your entire workforce, from hire to rehire.

Talent Management solutions built for growing and exceptional people

Built-in compliance tools that update with changing regulations

Automated payroll, attendance, and leave management

Insights that help HR leaders make faster, better decisions

Key Takeaways

- Leave encashment tax exemption under Section 10(10AA) applies only when encashment is received at retirement, resignation, or termination, not during active service.

- Government employees receive 100% tax exemption on leave encashment at retirement with no monetary cap.

- Private-sector employees receive a partial exemption capped at ₹25 lakh (lifetime, cumulative across all employers), calculated as the least of four statutory factors.

- The ₹25 lakh limit, introduced in Budget 2023, remains unchanged through FY 2025-26 and applies under both the old and new tax regimes.

- Enterprise HR teams benefit most from an online leave management system automating leave balance tracking, encashment calculations, and compliance documentation at scale.

- ZingHR's unified HCM platform, powered by Ghrowth.ai, its agentic intelligence engine, enables CHROs and CFOs to automate leave encashment compliance, generate board-ready analytics, and eliminate manual calculation errors across large, distributed workforces.

Introduction

Leave encashment becomes costly when HR, payroll, and finance treat it as a routine exit payout. A wrong exemption calculation under Section 10(10AA) can lead to excess TDS, Form 16 errors, employee disputes, and compliance risk during full-and-final settlement.

The 2023 Union Budget raised the exemption limit for private-sector employees from ₹3 lakh to ₹25 lakh, the first revision in over two decades. For CHROs, CFOs, and payroll heads, this makes updated leave policies, payroll logic, and settlement workflows essential for 2026.

The rules differ by employee type and timing. Government employees receive a full exemption at retirement. Private-sector employees get a partial exemption, capped at ₹25 lakh over their lifetime. Leave encashed during active service remains fully taxable.

This guide explains leave encashment tax exemption rules for 2026, including eligibility, calculation methods, new tax regime treatment, required documents, and how enterprise HR teams can reduce manual errors through automated leave management.

Leave Encashment Tax Exemption: Complete Comparison by Employee Category (2026)

The following table summarises how leave encashment tax exemption applies across every major scenario. Use this as a quick-reference framework before diving into the detailed sections below.

Leave encashment tax treatment by employee category, encashment timing, and applicable exemption limits under Section 10(10AA).

How Did We Compile This Guide?

The article draws directly from Section 10(10AA) of the Income Tax Act, 1961, relevant CBDT circulars (including Circular No. 8/2007), Supreme Court rulings (CIT vs. R.J. Shahney, CIT vs. M.P. State Electricity Board), and the Finance Act 2023 amendment raising the exemption limit to ₹25 lakh. All calculation examples follow the statutory "least-of-four" method. The goal is to provide an authoritative, enterprise-grade reference HR leaders, payroll managers, and tax professionals can rely on for policy design and ITR filing.

What Is An Leave Encashment Tax Exemption?

Leave encashment is the monetary compensation an employee receives for earned leave accumulated but not utilised during their tenure. Rather than forfeiting those unused leave days, the employee receives a cash payout, typically at retirement, resignation, or termination, though some organisations permit annual encashment during service as well.

Leave encashment tax exemption refers to the portion of the payout not subject to income tax. Under Indian tax law, the exemption is governed by Section 10(10AA) of the Income Tax Act, 1961, and its applicability depends on three variables: the employee's employer type (government vs. private), the timing of the encashment (during service vs. at exit), and the quantum of the payout relative to statutory limits.

The exemption framework operates as follows:

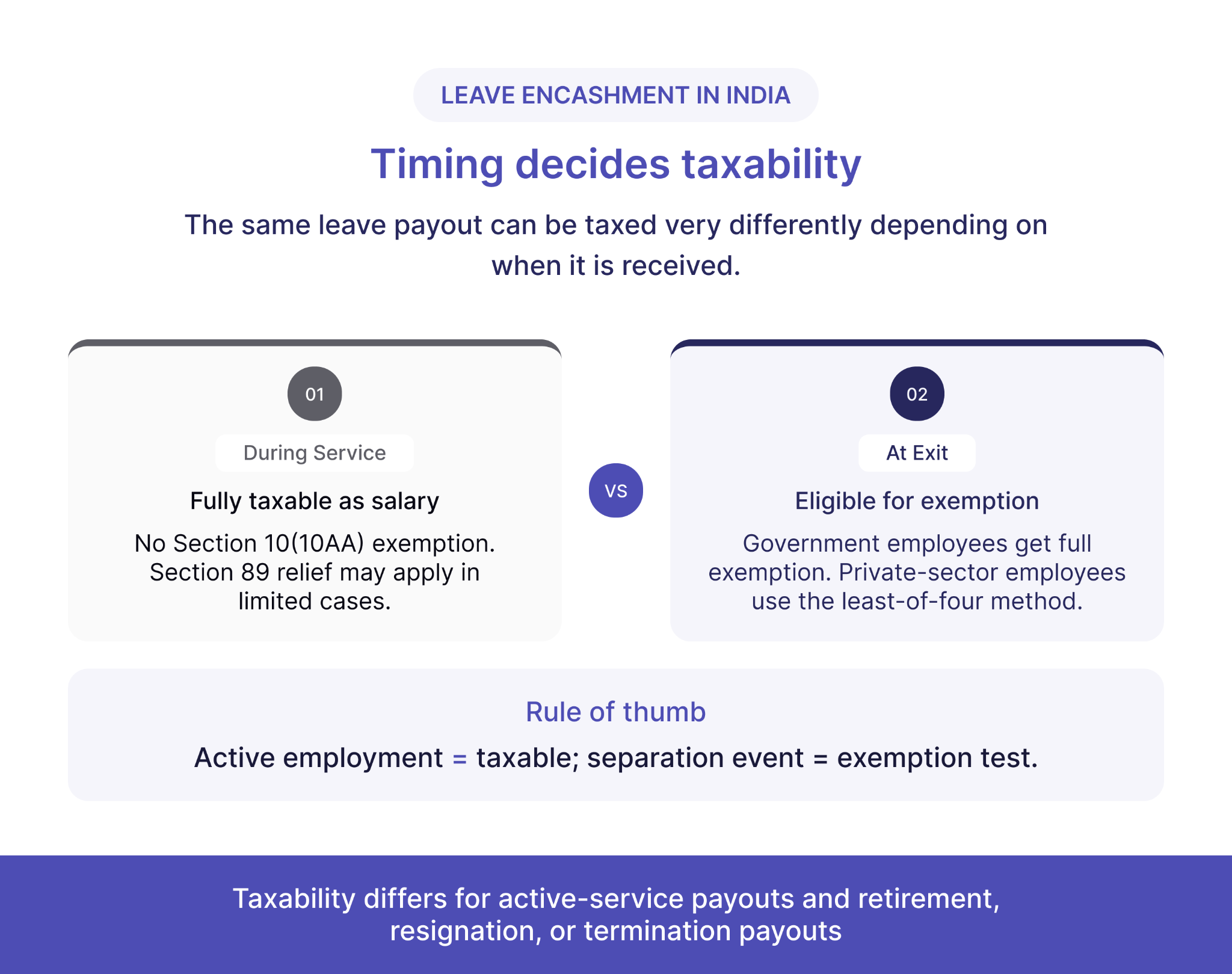

- During active service: Leave encashment is fully taxable as salary income. No exemption is available under Section 10(10AA), though Section 89 relief (via Form 10E) may reduce the tax burden if the encashment relates to arrears or accumulated service.

- At retirement, resignation, or termination: Leave encashment becomes eligible for exemption under Section 10(10AA).

- Government employees (Central or State): The entire amount received at retirement is 100% exempt from income tax, with no monetary cap.

- Private-sector employees: Exemption is partial, limited to the least of four calculated amounts, with a maximum cap of ₹25,00,000.

Understanding these distinctions matters for individual tax planning and for enterprise HR teams responsible for accurate full-and-final settlement processing, Form 16 generation, and compliance reporting. Organisations investing in digital HR transformation typically find automating these calculations eliminates the manual errors and inconsistencies leading to employee disputes and statutory non-compliance.

Budget Updates & Court Decisions on Leave Encashment

The recent legislative and judicial developments below shape how Section 10(10AA) applies in its current form. Two events stand out: the Finance Act 2023 amendment and a series of Supreme Court rulings stretching back to 1992.

1. Latest Budget Update (Finance Act 2023)

In the 2023 Union Budget, the government raised the leave encashment tax exemption limit for non-government employees from ₹3,00,000 to ₹25,00,000. The previous limit of ₹3 lakh had remained unchanged since 2002, through a period when average private-sector salaries increased several times over. The new limit, effective from FY 2023-24, brought meaningful tax relief to senior employees and long-tenured professionals in the private sector.

As of FY 2025-26 (the assessment year relevant to 2026 filings), the ₹25 lakh limit remains unchanged. No further revisions have been announced in subsequent budgets. The exemption applies only to encashment received at retirement, resignation, or termination. Leave encashed during active employment falls outside its scope.

2. Court Decisions and CBDT Circulars

Over the years, several landmark rulings and CBDT circulars have clarified the boundaries of leave encashment taxation:

- CIT vs. R.J. Shahney (1992): The Supreme Court held leave encashment received during active service is fully taxable as salary income. The ruling established the boundary between during-service and at-exit encashment, a distinction codified in all subsequent assessments.

- CIT vs. M.P. State Electricity Board (1992): The Supreme Court confirmed leave encashment received by government employees at retirement is fully exempt under Section 10(10AA).

- CBDT Circular No. 8/2007: The Central Board of Direct Taxes reiterated the exemption under Section 10(10AA) is applicable only when encashment is received on retirement or superannuation.

In short, the law draws a clear, judicially reinforced line. Leave encashed while working is fully taxable. Leave encashed at the end of employment is eligible for exemption, subject to the applicable limits for the employee's category.

Leave Encashment Exemption Under the Income Tax Law

Section 10(10AA) treats each employee category differently. The breakdown below covers the rules applicable to government employees, private-sector employees, and legal heirs of deceased employees.

Government Employees

If you are a Central or State Government employee, any leave encashment received at the end of your employment (whether through retirement, superannuation, or voluntary resignation) is 100% tax-free. There is no monetary ceiling. The full amount is exempt under Section 10(10AA)(i) and excluded from your taxable salary computation.

Private-Sector Employees

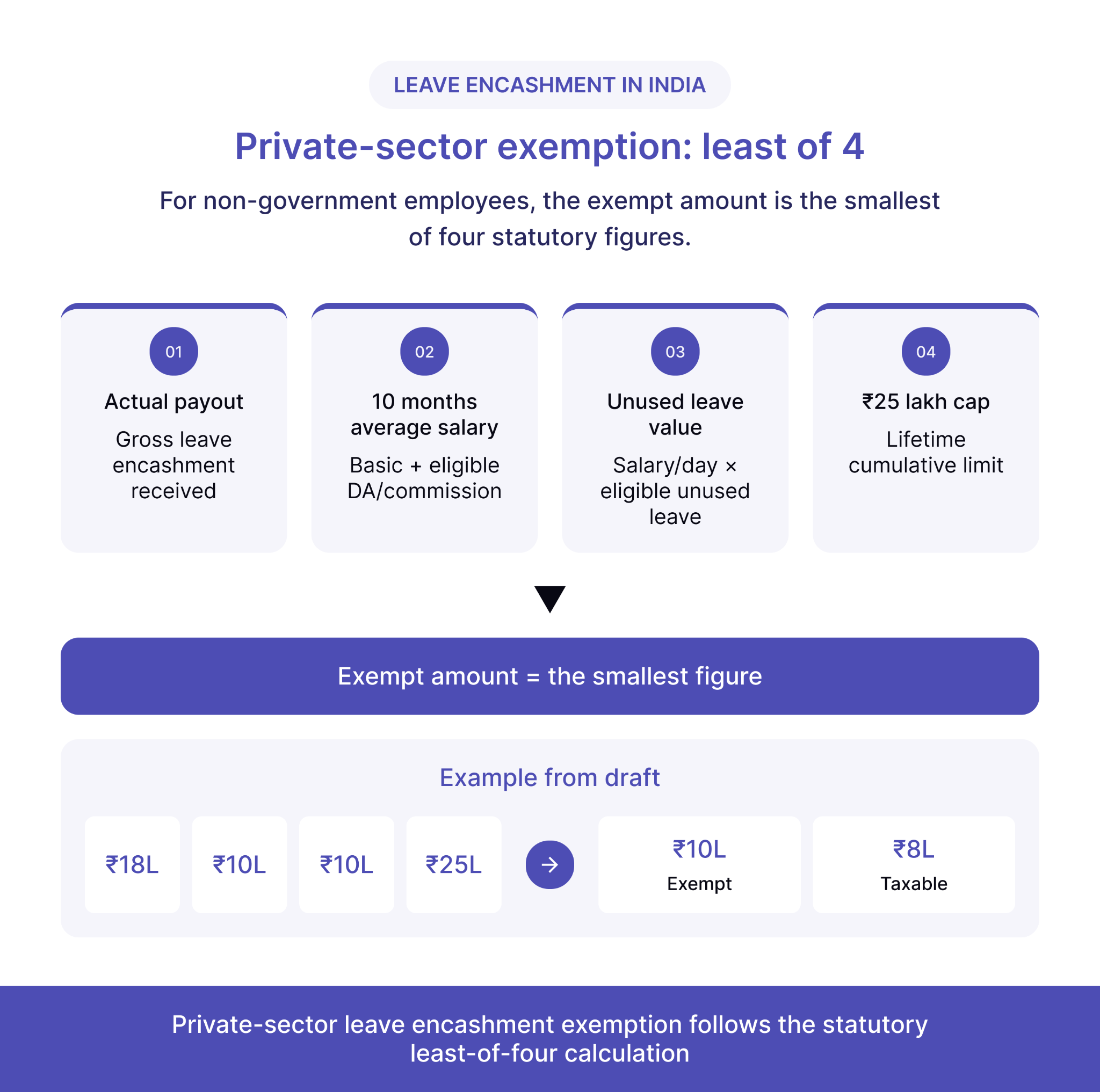

If you are a non-government employee, your leave encashment exemption at retirement, resignation, or termination is limited to the least of the following four amounts:

- Actual leave encashment received: the gross amount paid by your employer.

- 10 months' average salary: calculated as the average of your basic salary + dearness allowance (if forming part of retirement benefits) + commission (if a fixed percentage of turnover) over the last 10 months immediately preceding the date of retirement.

- Cash equivalent of unavailed leave: salary per day multiplied by unused leave days, capped at 30 days per completed year of service.

- ₹25,00,000: the statutory maximum (effective FY 2023-24 onwards).

Any amount received in excess of the least of these four figures is fully taxable as salary income and must be reported accordingly in the employee's Income Tax Return.

Legal Heirs of Deceased Employees

If leave encashment is received by the legal heir or nominee of a deceased employee, the entire amount is exempt from income tax, regardless of whether the deceased was a government or private-sector employee. The exemption carries no monetary cap.

Leave Encashment Taxability: During Service vs. At Exit

Leave encashed while still employed and leave encashed at separation follow different tax treatments, and the consequences of confusing them show up in TDS miscalculations and Form 16 discrepancies.

Leave Encashment During Active Service

Leave encashment received during service, while you are still employed by the organisation, is fully taxable. The entire amount is added to your gross salary for the relevant financial year and taxed at your applicable income tax slab rate.

Example: If you receive ₹1,00,000 as annual leave encashment while still employed, the full ₹1,00,000 is taxable. No exemption under Section 10(10AA) is available.

If the during-service encashment creates a disproportionate tax burden because it relates to leave accumulated over multiple years, you may claim relief under Section 89 of the Income Tax Act by filing Form 10E on the income tax e-filing portal. Form 10E recalculates the tax as though the income were spread across the years in which the leave was earned.

Leave Encashment at Retirement, Resignation, or Termination

Leave encashment received at the end of employment (retirement, superannuation, resignation, or termination) is eligible for exemption under Section 10(10AA).

- Government employees: Full exemption, no cap.

- Private-sector employees: Partial exemption, limited to the least of the four factors described above. The exempt portion is excluded from taxable salary; the balance is included.

Optimise Leave Management

Automate and simplify leave management with ZingHR's integrated solutions.

Leave Encashment Calculation Formula: Step-by-Step

The four-factor calculation under Section 10(10AA) generates the most compliance risk for enterprise payroll teams. The methodology below breaks down each step in the sequence the calculation must follow.

Formula for Private-Sector Employees

Exempt Amount = the LEAST of:

- Actual leave encashment received

- 10 months' average salary

- Cash equivalent of unavailed leave (salary per day × unused leave days, max 30 days per completed year of service)

- ₹25,00,000

Defining "Average Salary"

Average salary for the purpose of this calculation includes:

- Basic salary averaged over the last 10 months immediately preceding retirement/resignation

- Dearness Allowance (DA): only if it forms part of retirement benefits

- Commission: only if it is a fixed percentage of turnover

Excluded components: HRA, conveyance allowance, special allowance, bonus, overtime, and any other allowances are not included in the average salary computation.

Worked Example: Leave Encashment Exemption Calculation

Scenario: Mr. Yogesh Sharma, a private-sector employee, retires on 31 March 2026 after 20 years of service. He has accumulated 300 days of unused earned leave. His monthly basic salary plus DA averaged ₹1,00,000 over the last 10 months. His employer pays ₹18,00,000 as leave encashment.

Step 1: Actual leave encashment received: ₹18,00,000

Step 2: 10 months' average salary: ₹1,00,000 × 10 = ₹10,00,000

Step 3: Cash equivalent of unavailed leave:

- Maximum allowed leave: 30 days × 20 years = 600 days

- Actual unused leave: 300 days (lower of 600 and 300)

- Salary per day: ₹1,00,000 ÷ 30 = ₹3,333.33

- Cash equivalent: 300 days × ₹3,333.33 = ₹10,00,000

- Alternatively: (300 ÷ 30) × ₹1,00,000 = 10 × ₹1,00,000 = ₹10,00,000

Step 4: Statutory maximum: ₹25,00,000

Exempt amount = Least of (₹18L, ₹10L, ₹10L, ₹25L) = ₹10,00,000

Taxable amount: ₹18,00,000 − ₹10,00,000 = ₹8,00,000

Mr. Yogesh must include ₹8,00,000 in his taxable salary income for FY 2025-26. The remaining ₹10,00,000 is exempt under Section 10(10AA).

Exemption Limit & Conditions

The quantum of leave encashment exemption a private-sector employee can claim depends on several inter-related variables. Understanding each factor prevents miscalculations at exit and ensures the organisation's payroll team processes full-and-final settlements within the statutory framework.

Maximum Exemption Limit

The statutory ceiling for leave encashment tax exemption for non-government employees is ₹25,00,000, effective from FY 2023-24. The limit remains unchanged through FY 2025-26.

Factors Affecting Exemption Eligibility

Enterprise HR teams must account for the following variables when processing leave encashment:

- Type of employer: Government employees receive full exemption. Private-sector employees receive partial exemption.

- Completed years of service: Determines the maximum leave days eligible for calculation (30 days per completed year).

- Unavailed leave balance: Only unused earned/privileged leave qualifies. Casual leave and sick leave are generally excluded.

- Salary components: Only basic salary, DA (if part of retirement benefits), and commission (percentage of turnover) are included.

- Timing of encashment: Must be received at retirement, resignation, or termination to qualify for exemption.

- Prior exemptions claimed: The ₹25 lakh limit is cumulative across all employers throughout an employee's career. If an employee claimed ₹10 lakh exemption from Employer A, only ₹15 lakh remains available at Employer B.

Leave Encashment Exemption Under the New Tax Regime

Many employees in 2026 assume switching to the new tax regime forfeits leave encashment exemption. Section 10(10AA) exemption is available under both the old and new tax regimes. Deductions under Chapter VI-A, such as Section 80C, do not carry across regimes. The Section 10(10AA) exemption operates independently of regime selection, and employees may claim it regardless of which regime they choose.

For during-service encashment, Section 89 relief (Form 10E) remains primarily beneficial under the old regime. Employees should consult a tax professional to determine the most advantageous regime for their overall income profile.

How to Claim Leave Encashment Exemption

Claiming leave encashment exemption requires accurate reporting in the ITR and close coordination between the employee and the employer's payroll team. The steps and required documents below apply to private-sector employees receiving encashment at exit.

Steps to Claim Leave Encashment Exemption in Your ITR

- Obtain Form 16 from your employer: the leave encashment amount should be reported as a separate line item under salary income.

- Verify "Salary Income" details: confirm the gross leave encashment amount and any exempt portion already reflected by the employer.

- Log in to the Income Tax e-Filing portal and navigate to the "Salary" section of your ITR form (ITR-1 or ITR-2, as applicable).

- Report the full leave encashment received as part of gross salary.

- Claim exemption under Section 10(10AA) by entering the exempt portion in the designated field. The system will automatically compute the taxable balance.

- If applicable, file Form 10E for Section 89 relief (relevant for during-service encashment taxed in a single year).

- Verify, preview, and e-file your return. The taxable portion of leave encashment is included in gross salary for slab-rate taxation.

Required Documents

- Form 16 or Salary Certificate: showing leave encashment as a separate salary component

- Leave Balance Certificate: issued by HR, confirming accumulated unused leave days

- Computation sheet: some employers issue a detailed exemption calculation sheet

- Bank statement: showing the credit of the leave encashment amount

- Employment proof: appointment letter, employee ID, or relieving letter (if required by the assessing officer)

These documents do not need to be attached to the ITR at the time of filing, but they must be retained for a minimum of six years in case of scrutiny or reassessment.

For enterprise HR teams processing hundreds or thousands of separations annually, maintaining accurate leave records and generating compliant Form 16s at scale requires a systematic approach. Organisations using cloud HRMS benefits find automated leave tracking, policy-engine-driven encashment calculations, and integrated payroll ensure statutory accuracy without manual intervention.

Benefits of Automated Leave Encashment Management

Manual leave encashment processing across large workforces exposes organisations to calculation errors, settlement backlogs, and audit risk. The five operational benefits below demonstrate why automated leave management systems deliver measurable value for enterprises managing separations at scale.

1. Elimination of Manual Calculation Errors

The four-factor "least of" calculation under Section 10(10AA) requires accurate data on leave balances, salary components, years of service, and prior exemptions. When performed manually across hundreds of employees, errors are inevitable. Automated leave management systems perform these calculations instantly, pulling verified data from integrated HRMS and payroll modules. Automated systems eliminate the discrepancies leading to incorrect Form 16 issuance, employee grievances, and adverse tax assessments.

2. Compliance Consistency Across Geographies

Enterprises operating across multiple Indian states must ensure uniform application of leave encashment tax rules, even as state-specific labour laws (such as the Shops and Establishments Act) vary on leave accumulation caps and carry-forward rules. A centralised, policy-engine-driven system ensures encashment calculations comply with both central tax law and state-level labour regulations, a requirement for industries like BFSI, Pharma, and Manufacturing.

3. Real-Time Liability Visibility for CFOs

Accumulated unused leave represents an accrued financial liability. For publicly listed enterprises and those following Ind-AS accounting standards, accurate provisioning for leave encashment liabilities is a reporting requirement. Automated systems provide real-time dashboards showing leave liability across departments, business units, and locations, enabling CFOs to make informed provisioning decisions and avoid year-end surprises.

4. Faster Full-and-Final Settlements

Leave encashment is a significant component of full-and-final settlements during resignation or retirement. Delays in calculating the exempt and taxable portions lead to settlement backlogs, delayed final payments, and poor employee exit experiences. Automation reduces settlement processing time from days to hours, supporting positive employer branding even at the point of separation.

5. Audit Readiness and Documentation

Income tax authorities may scrutinise leave encashment exemption claims, particularly for large payouts. Maintaining a complete audit trail covering leave balance history, salary records, calculation methodology, and prior employer exemptions is essential. Automated systems generate and archive this documentation systematically, keeping the organisation audit-ready.

Key Features of Modern Leave Management Software

Enterprise leave management software must handle more than basic leave tracking. The six capabilities below define what a purpose-built system needs to address for organisations managing complex leave policies, multi-entity payroll, and statutory compliance.

1. Configurable Leave Policy Engine

Enterprises need the ability to define multiple leave types (earned leave, casual leave, sick leave, compensatory off) with distinct accumulation, lapsing, and encashment rules, configurable by employee grade, department, location, and entity. The policy engine should automatically enforce caps (e.g., 30 days per year for earned leave) and flag discrepancies.

2. Automated Encashment Calculation Module

The software should calculate leave encashment exemption using the statutory "least-of-four" method, automatically pulling salary data, leave balances, and service tenure from integrated modules. The module must support both at-exit and during-service encashment scenarios, applying the correct tax treatment to each.

3. Cumulative Exemption Tracking Across Employers

Given the ₹25 lakh lifetime cap applies cumulatively across all employers, the system should allow HR teams to record exemptions claimed at previous employers (as declared by the employee at onboarding) and adjust the available exemption accordingly. The requirement is particularly critical for enterprises hiring mid-career professionals.

4. Integration with Payroll and Tax Filing

Leave encashment data must feed directly into payroll processing and Form 16 generation. The software should compute TDS on the taxable portion, reflect the exempt portion in the correct Form 16 field, and support bulk generation for large employee populations. Integration with HR and automation analytics platforms provides CHROs with data-driven insights into leave utilisation patterns and encashment trends.

5. Regulatory Update Management

Tax rules and exemption limits can change with each Finance Act. The software must incorporate regulatory updates promptly, such as the ₹3 lakh to ₹25 lakh revision in FY 2023-24, without requiring manual reconfiguration. Enterprises prioritising an HR tech rehaul ensure their systems remain current without operational disruption.

6. Self-Service Employee Portal

Employees should be able to view their leave balances, simulate encashment amounts, and understand the tax implications through a self-service portal. A self-service portal reduces HR query volumes, improves transparency, and gives employees the information to make informed decisions about leave utilisation versus encashment.

Why Choose ZingHR for Leave Encashment Compliance?

ZingHR is a strategic command centre for enterprise HR, engineered for Boards, CHROs, CFOs, and CXOs requiring unified workforce intelligence and airtight compliance at scale. ZingHR's unified HCM platform, powered by Growth.ai, its agentic intelligence engine, automates the entire leave encashment lifecycle: from real-time leave balance tracking and configurable policy engines to statutory encashment calculations, payroll integration, and Form 16 generation, all within a single cloud-based HR software ecosystem.

For enterprises in regulated industries such as BFSI, Pharma, and Manufacturing, ZingHR delivers compliance assurance beyond fragmented or legacy HR systems. The platform supports multi-entity, multi-location leave policies, enforces state-specific labour law requirements alongside central tax regulations, and provides board-ready analytics on leave liability, encashment trends, and workforce productivity metrics. ISO 27001 certified and trusted by leading enterprises across India, ZingHR ensures your leave encashment processes are accurate, auditable, and aligned with the latest statutory framework.

If your organisation is ready to move beyond manual spreadsheets and disconnected payroll modules, digitising HR with ZingHR delivers measurable outcomes: faster settlements, zero-error exemption calculations, reduced compliance risk, and a superior employee experience from onboarding to exit.

Get Leave Encashment Compliance Right Before the Next Exit

Leave encashment tax exemption carries direct financial and compliance weight for every employee planning their exit and every enterprise processing separations at scale. The core principles are straightforward once absorbed:

- Timing determines eligibility. Encashment at retirement or resignation qualifies for exemption. Leave encashed during service carries no exemption.

- The "least-of-four" calculation protects lower earners while capping the benefit at ₹25 lakh, ensuring proportional tax relief across salary levels and service tenures.

- The ₹25 lakh lifetime cap is cumulative. Employees who change employers multiple times must track exemptions claimed at each exit to avoid over-claiming, and employers must record this at onboarding.

- Both tax regimes honour this exemption. Section 10(10AA) applies under the old and new tax regimes, removing a common misconception deterring employees from regime selection.

- Enterprise HR automation eliminates risk. Manual calculations across large workforces invite errors, disputes, and scrutiny. An integrated, policy-driven leave management platform (such as ZingHR's unified HCM) ensures every encashment is computed, documented, and reported accurately.

Individual employees optimising their tax returns and CHROs overseeing compliance for thousands of separations annually will find the rules outlined in this guide an authoritative framework for 2026 and beyond.

Why Choose ZingHR for Leave Encashment Compliance?

ZingHR is the AI-powered Hire-to-Retire platform built to remove transactional HR from enterprise operations permanently.

Its leave management and payroll modules run on a single codebase and database, which means leave balances, salary data, service tenure, and exemption history all feed into one calculation engine without manual handoffs.

- Ghrowth.ai, its agentic intelligence engine: Surfaces leave liability trends, flags encashment anomalies, and provides board-ready analytics on workforce separation costs, without HR teams pulling reports manually. CHROs and CFOs see the full picture in real time.

- Automated least-of-four calculation: The platform computes Section 10(10AA) exemption automatically, pulling verified salary components, leave balances, years of service, and prior employer exemptions from integrated modules. Every figure is auditable and traceable to its source.

- Cumulative exemption tracking across employers: The ₹25 lakh lifetime cap applies across every employer in an employee's career. ZingHR captures prior exemption declarations at onboarding and adjusts the available exemption accordingly, closing the gap where most manual processes fail.

- Built-in compliance for regulated industries: BFSI, Pharma, Manufacturing, and Healthcare organisations get state-specific labour law enforcement alongside central tax rules, within the same system. Multi-entity, multi-location leave policies run from one configuration layer.

- Full-and-final settlement at speed: Leave encashment calculations, TDS deductions, and Form 16 generation run within a single workflow. Settlement processing time drops from days to hours, with a complete audit trail retained automatically for scrutiny or reassessment.

- ISO 27001 certified infrastructure: All leave records, salary data, and exemption documentation are stored on ZingHR's ISO 27001:2022 certified cloud, hosted on Microsoft Azure with AES 256-bit encryption and role-based access controls.

Over 1,200 enterprises across India, MEA, and SEA use ZingHR to process separations accurately at scale.

Book a demo with ZingHR to see how the platform handles leave encashment compliance for your workforce size and industry.

Frequently asked questions (FAQs)

Non-government employees can claim a maximum tax exemption of ₹25,00,000 on leave encashment received at retirement or resignation under Section 10(10AA). The limit increased from ₹3,00,000 in Budget 2023 and remains unchanged through FY 2025-26. Any amount exceeding ₹25 lakh is taxable as salary income. The cap is a lifetime cumulative limit: it applies across all employers throughout your career, not per employer or per financial year.

Leave encashment received during active service is fully taxable and added to your salary income at your regular slab rate. The exemption under Section 10(10AA) applies only when encashment is received at retirement, resignation, or termination. If during-service encashment creates a disproportionate tax burden because it relates to leave accumulated over multiple years, you can claim relief under Section 89 by filing Form 10E on the income tax e-filing portal, which recalculates your tax liability as if the income were spread across the relevant years.

The exempt amount is the least of four factors: (1) ₹25,00,000, (2) actual leave encashment amount received, (3) average salary of the last 10 months (basic + DA + qualifying commission), and (4) salary per day multiplied by unused leave days, capped at 30 days per completed year of service. For example, if your average monthly salary is ₹80,000 and you have 15 years of service with 200 unused days, the calculation evaluates each factor and applies the lowest result as your exempt amount. The balance is fully taxable.

Government employees (Central and State) receive full tax exemption on leave encashment at retirement, with no monetary cap, under Section 10(10AA)(i). Private-sector employees receive partial exemption, capped at ₹25,00,000 and subject to the four-factor calculation. When leave encashment is paid to the legal heir of a deceased employee (whether government or private), the entire amount is 100% tax-free, regardless of any limit.

Yes. Section 10(10AA) exemption is available under both the old and new tax regimes. The Section 10(10AA) exemption is regime-neutral, unlike Chapter VI-A deductions such as Section 80C. You may claim it regardless of regime selection. For during-service encashment where you are seeking Section 89 relief via Form 10E, the comparative benefit may vary by regime. Consult a tax professional to determine which regime optimises your overall tax position.

The ₹25,00,000 exemption limit is cumulative across all employers, both within the same financial year and across your entire career. If you received ₹15,00,000 from Employer A and ₹12,00,000 from Employer B in the same year, your total exemption is capped at ₹25,00,000, meaning ₹2,00,000 would be taxable. If you had already claimed ₹10,00,000 exemption at a previous employer years earlier, only ₹15,00,000 of exemption remains available for all future employers combined. Tracking cumulative exemptions is essential, and enterprise HR teams should capture this data during the onboarding process through self-declaration forms.

What to do next?

See ZingHR in Action

Join the 1,200+ enterprises that have replaced fragmented HR with one intelligent, future-ready platform. See ZingHR in 30 minutes.

Build the Organization You Want

Great HR drives retention, capability, and culture. ZingHR takes care of the operational layer so your people team owns the strategy.

Elevating Impact.

Defining Destiny

See how ZingHR's AI-powered Hire-to-ReHire platform frees your CPO to lead with purpose and deliver the outcomes your Board is watching for

ZingHR is the AI-powered Hire-to-ReHire platform built for one purpose to remove every transactional layer of HR from your organisation, permanently.